iklan2

When I first started trading at the ripe age of 15 years old, it was because I had lost over $3,000 of my roughly $5,000 in life savings from mowing lawns in the dotcom crash. The mutual funds my parents had invested me in had plummeted in value.

As a result of this traumatic experience, I wanted to take charge of my financial future and not leave it in the hands of an actively managed mutual fund.

With no concept of trading costs, order execution quality, let alone a fear for losing, I sold the mutual funds, opened a custodian account at TD Ameritrade, and quickly started crushing the market.

Over the course of three years I took my portfolio of several thousand and ran it up to nearly $100,000.

I was the man.

When I reached my peak portfolio value at age 18, I was a freshman in college with three monitors on my dorm room desk, skipping class and day trading for friends live. See: Tools of the ‘Trade’ – How I Invest (2018 Edition).

I then lost $72,000 in one trade and realized there was a lot more to trading than meets the eye.

Now at the ripe old age of 31, 16 years of market “experience” has helped me realize that I was a statistic in a game that never ends.

Just like rolling heads ten times in a row, my luck streak ran out and I gave most of what I had earned back to the market.

Looking back, here are ten hard facts I wish I had understood when I got started.

The dream advertised by stock picking subscription services, instagram accounts, and the like are all built on a foundation of sand.

Sadly, it’s all clever marketing and not a reality.

FACT: 99.9% of stock picking service providers make more money from their subscriptions and product sales than they do their own trading.

They are able to live the “lifestyle” because of you and your desire to day trade part-time or make some money on the side or get rich investing. Without you, the vast majority of stock picking services wouldn’t exist.

The next time you see a trading service trying to sell you on a DVD, subscription, or trading course, look around the site and see if they have audited tax records of their returns listed anywhere. They won’t. See: Top 20 Recommended Investing Books.

The only difference between you and them is that they figured out #9 and #8 below before you and decided to pursue a career in education and “giving back” to help you out. This includes sharing their daily stock picks and lessons for a monthly fee.

Lesson: Professional trading is not for the faint of heart and rarely includes the “lifestyle” portrayed by the web.

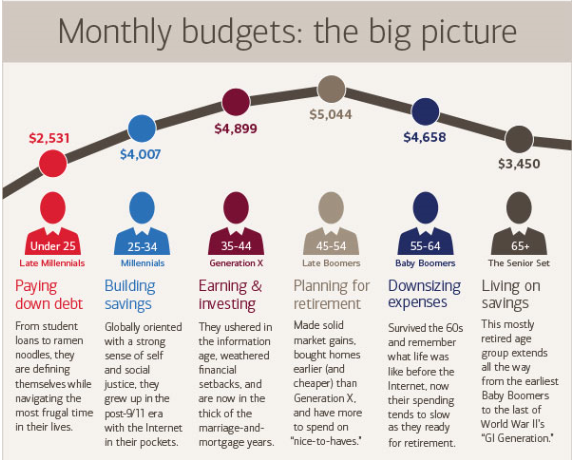

When you’re young and single, you can keep costs down. Heck, I was living on less than a $100 per month food budget at one point to pursue the dream. According to the United States Bureau of Labor Statistics, the average American under 25 spends $2,531 per month or $30,372 per year.

As you age, your expenses naturally go up.

Now you may thinking, “Blain, there is thing called leverage.”

Yes, there are ways to leverage your portfolio. With $25,000 margin account and pattern day trader status, you could theoretically trade up to $100,000 (4x) in securities per day and hold up to $50,000 (2x) overnight. It’s a gift and a curse. The stakes are much higher.

Looking at some basic math, let’s say your single and under 25. Your cost of living should be on average $30,372 per year and your tax rate is effectively zero.

To break even on a $1 million portfolio, you would need to return 3.1% a year. With a $100,000 portfolio, you are talking about a 31% return.

Again, just to break even.

Mind you, this doesn’t include trading costs, research, trading subscriptions, etc. which can easily total thousands of dollars a year.

Even if you had an unbelievable year and returned 50% on a $100,000 portfolio, you are only building your bankroll +$14,769 for next year ($50,000 – $4,859 taxes – $30,372 avg cost of living). Again, not including trading costs.

If that wasn’t daunting enough, the above assumes you never have a down month or year.

To live you need to take draws every month (another piece of wisdom I realized after the fact), which means you need to win… constantly. Shrinking your portfolio base even 10% is a serious hurdle to overcome.

Lesson: You can get started with as little as a few thousand dollars, but don’t get suckered into attempting to trade for a living unless you have at least a $1,000,000 portfolio. When you factor in the swings of trading, taxes, cost of living, and time, its seriously david vs goliath math.

YOU: Go to the mall on the weekend, walk into a Lululemon store, see a lot of people paying full price for yoga pants. The “aha” moment, this place is packed. You use your mobile trading app to scan a tag, discover “LULU” as the ticker symbol, talk to the sales clerk about how sales have been, then quickly buy some shares on your phone.

INSTITUTIONAL FUND: Knows the founders and has regular calls with the CFO. Their research staff calls Lululemon stores across the country, as well as suppliers, and pulls data nationwide to determine how the numbers are really lining up. They then analyze to determine that margins are being contracted despite strong sales growth and sell the stock heading into its next earnings call.

To take this full circle, guess what happened to Lululemon after it’s most recent earnings DESPITE positive chatter from traders and analysts? -16.41% the next day.

Here’s what one research group, FBR Capital, had to say post Lululemon earnings:

Is that what your research pulled up too? Doubt it.

Lesson: Don’t ever think for a second that you can outsmart the market. There is always someone out there that knows more than you.

Allocate no more than 5% of your portfolio to personal trading and invest the rest in low cost index funds.

An oldie but a goody, the Wall Street Journal had a weekend feature back in 2013 titled, Investing for the Fun of It. Here’s an excerpt:

Lesson: Your long term future is more important than your short term desire to get rich overnight. Trade with no more than 5% of your portfolio and invest the rest in low cost index funds.

To understand this concept, Investopedia explains it best in this video:

Let’s run some hypothetical examples.

Example A: $10,000 starting portfolio, $2,000 added per year with a 5% return per year.

After 35 years, total contributions equal $80,000. End portfolio value, $235,800.77. Gross return, +$155,000 (+195%).

Example B: $10,000 starting portfolio, $2,000 added per year with a 9.6% return per year (S&P 500 historical return).

After 35 years, total contributions equal $80,000. End portfolio value, $741,930.11. Gross return, +$661,930.11 (+827%).

Looking at scenario B with a 4.6% higher annual return, the difference is a staggering $506,129.34.

Fun fact: over any 20 year period since 1926, the S&P 500 has never returned a loss.

Lesson: The earlier you can start investing (ideally in low cost index funds), the better. The power of compounded returns over the course of several decades cannot be underestimated.

Unfortunately, ads like the one above for penny stocks are designed to sucker you in to buy a product or service. These tips are utter junk and will leave your wallet and portfolio bleeding red in the end.

Reality: If someone even had a strategy that could consistently return even 11% per year, they’d be rich beyond their wildest dreams and would not need to sell picks.

The S&P 500 historical return is 9.6%. Endowments, pension funds, and the like would poor money hand over fist into any fund manager that could consistently generate 1.4% of alpha decade after decade.

Lastly, this rule includes Wall Street analysts. Ignore analyst buy/sell recommendations.

No one knows what the market is going to do tomorrow, next week, or next year. At best, it’s just an “educated guess” from someone really “smart”.

Warren Buffett sums it up best,

Lesson: No matter how smart they are, the odds are always stacked against you. Pursue stock tips with extreme skepticism.

The opposite is also true. Make a great call, follow your rules, and sell a monster winner that represents over 90% of your gains for the year. Despite dozens or hundreds of uneventful trades over months prior, you’ll be very happy you showed up ready to trade that day.

Lesson: Never underestimate the impact a single trade decision can have on your portfolio.

Out performing the S&P 500 in any given year is a feat in itself, but when you then take into consideration taxes, commission costs, and research (those hot stock pick services, chat rooms, and market newsletters don’t come for free), the game becomes that much more difficult.

Lesson: When taxes, commissions, and other costs of trading such as research are taking into consideration, the challenge of outperforming the market year after year as a career are compounded.

2. Confirmation bias and your emotions are your worst enemy

Confirmation bias definition via Wikipedia,

In the trading world, this means you see a setup or price action and quickly convince yourself to buy or sell. Unfortunately, 99% of the time you should be doing the direct opposite.

Technical analysis is one of the worst in provoking this natural human behavior. “Oh, I’ve seen this pattern before, it’s a buy”. There is a reason why online brokers offer dozens and in some cases hundreds of technical indicators. Indicators encourage you to see more “patterns” and trade more frequently.

In poker, a player can go on “tilt” and make poor decisions, ultimately losing their stack in a hurry. The same mental dilemma applies to trading.

Several quotes from market masters on trading psychology,

Lesson: Trading is 90% mental and 10% skill. Those who succeed learn to manage risk and trade unemotionally.

Historically speaking, since 1928 the S&P 500 has returned 9.6% per year. By simply buying an ETF like SPY or VOO, you can replicate the performance of the S&P 500 for .09% or .05%, respectively, in expense ratios per year. The same applies for mutual funds like Vanguard’s VFIAX.

As far as allocation goes, Warren also keeps it simple,

The numbers don’t lie. Despite staffs of analysts, access to CEOs, CFOs, unlimited capital for research, etc. on average, the majority of hedge funds underperform the market each year.

For a detailed guide on passive indexing like Warren Buffett, see How to Build a Warren Buffett Portfolio.

Lesson: Warren Buffett is the greatest investor of all-time. He recommends low cost indexing, instead of market timing, as the best path to long term success.

While I have no regrets of investing thousands of hours into the markets over the past 14 years, I’ve had to accept the reality that my retirement portfolio would be further ahead had I understood these truths from the beginning:

If your mentality is to use the market as a vehicle to supplement income or get rich because you don’t see your personal career getting you where you want to be, stop yourself, you’re already primed for failure.

As a result of this traumatic experience, I wanted to take charge of my financial future and not leave it in the hands of an actively managed mutual fund.

With no concept of trading costs, order execution quality, let alone a fear for losing, I sold the mutual funds, opened a custodian account at TD Ameritrade, and quickly started crushing the market.

Over the course of three years I took my portfolio of several thousand and ran it up to nearly $100,000.

I was the man.

When I reached my peak portfolio value at age 18, I was a freshman in college with three monitors on my dorm room desk, skipping class and day trading for friends live. See: Tools of the ‘Trade’ – How I Invest (2018 Edition).

I then lost $72,000 in one trade and realized there was a lot more to trading than meets the eye.

Now at the ripe old age of 31, 16 years of market “experience” has helped me realize that I was a statistic in a game that never ends.

Just like rolling heads ten times in a row, my luck streak ran out and I gave most of what I had earned back to the market.

Looking back, here are ten hard facts I wish I had understood when I got started.

10. The “lifestyle” of a pro trader is a big fat lie

Yachts, women (men for those ladies pursuing the dream), private jets and business class, presidential suites, fancy cars, 10k stacks, mansions, etc all encompass what is presented as the “dream day trader lifestyle”.

The dream advertised by stock picking subscription services, instagram accounts, and the like are all built on a foundation of sand.

Sadly, it’s all clever marketing and not a reality.

FACT: 99.9% of stock picking service providers make more money from their subscriptions and product sales than they do their own trading.

They are able to live the “lifestyle” because of you and your desire to day trade part-time or make some money on the side or get rich investing. Without you, the vast majority of stock picking services wouldn’t exist.

The next time you see a trading service trying to sell you on a DVD, subscription, or trading course, look around the site and see if they have audited tax records of their returns listed anywhere. They won’t. See: Top 20 Recommended Investing Books.

The only difference between you and them is that they figured out #9 and #8 below before you and decided to pursue a career in education and “giving back” to help you out. This includes sharing their daily stock picks and lessons for a monthly fee.

Lesson: Professional trading is not for the faint of heart and rarely includes the “lifestyle” portrayed by the web.

9. You really need at least a $1,000,000 portfolio to trade full-time

To trade for a living, you need a larger bankroll because it isn’t just factoring for winning as well as losing years, you have to cover trading expenses, draw a salary, and pay bills alongside taxes on capital gains.When you’re young and single, you can keep costs down. Heck, I was living on less than a $100 per month food budget at one point to pursue the dream. According to the United States Bureau of Labor Statistics, the average American under 25 spends $2,531 per month or $30,372 per year.

As you age, your expenses naturally go up.

Now you may thinking, “Blain, there is thing called leverage.”

Yes, there are ways to leverage your portfolio. With $25,000 margin account and pattern day trader status, you could theoretically trade up to $100,000 (4x) in securities per day and hold up to $50,000 (2x) overnight. It’s a gift and a curse. The stakes are much higher.

Looking at some basic math, let’s say your single and under 25. Your cost of living should be on average $30,372 per year and your tax rate is effectively zero.

To break even on a $1 million portfolio, you would need to return 3.1% a year. With a $100,000 portfolio, you are talking about a 31% return.

Again, just to break even.

Mind you, this doesn’t include trading costs, research, trading subscriptions, etc. which can easily total thousands of dollars a year.

Even if you had an unbelievable year and returned 50% on a $100,000 portfolio, you are only building your bankroll +$14,769 for next year ($50,000 – $4,859 taxes – $30,372 avg cost of living). Again, not including trading costs.

If that wasn’t daunting enough, the above assumes you never have a down month or year.

To live you need to take draws every month (another piece of wisdom I realized after the fact), which means you need to win… constantly. Shrinking your portfolio base even 10% is a serious hurdle to overcome.

Lesson: You can get started with as little as a few thousand dollars, but don’t get suckered into attempting to trade for a living unless you have at least a $1,000,000 portfolio. When you factor in the swings of trading, taxes, cost of living, and time, its seriously david vs goliath math.

8. The odds are stacked against you

There are many very smart people out there. With a global stock market cap of $69 trillion, there is a lot of money at stake and endless resources put into research.YOU: Go to the mall on the weekend, walk into a Lululemon store, see a lot of people paying full price for yoga pants. The “aha” moment, this place is packed. You use your mobile trading app to scan a tag, discover “LULU” as the ticker symbol, talk to the sales clerk about how sales have been, then quickly buy some shares on your phone.

INSTITUTIONAL FUND: Knows the founders and has regular calls with the CFO. Their research staff calls Lululemon stores across the country, as well as suppliers, and pulls data nationwide to determine how the numbers are really lining up. They then analyze to determine that margins are being contracted despite strong sales growth and sell the stock heading into its next earnings call.

To take this full circle, guess what happened to Lululemon after it’s most recent earnings DESPITE positive chatter from traders and analysts? -16.41% the next day.

Here’s what one research group, FBR Capital, had to say post Lululemon earnings:

“Firm notes the key 2Q issue was the GM miss relative to guidance/expectations, which reflected incremental port-delay-related/material liability costs and potentially a greater-than-expected mix shift to lower-margin categories (men’s, women’s fashion). Of foremost go-forward concern is a +55% increase in inventories, which, in addition to sales higher-cost units, is likely a factor in its lower 3Q guide relative to the Street. While there is some in-transit/early delivery noise, LULU has to move through a significant amount of product in 2H15 to normalize sales/inventories.”

Lesson: Don’t ever think for a second that you can outsmart the market. There is always someone out there that knows more than you.

7. The 5% rule

Allocate no more than 5% of your portfolio to personal trading and invest the rest in low cost index funds.An oldie but a goody, the Wall Street Journal had a weekend feature back in 2013 titled, Investing for the Fun of It. Here’s an excerpt:

Win or lose, the key to using play money safely is to make sure it involves a sum the investor can live without.

“Enjoy the fun of gambling and the thrill of the chase, but not with your rent money and certainly not with college education funds for your children, nor with your retirement nest egg,” John Bogle, Vanguard’s founder, wrote in “The Little Book of Common Sense Investing,” published in 2007.

Mr. Bogle wrote that what he called “funny money” should amount to no more than 5% of a person’s investments. Some experts put the limit lower. Mr. Malkiel says it depends upon the investor’s individual circumstances.

Getting the proportion wrong is one risk. Another is that an investor will lose, for example, 5% of his or her money and think, “I was so, so close. Let me take another 5%,” Mr. Statman says. The temptation to keep on trying to win is common, he says, and some people find it hard to resist.

Lesson: Your long term future is more important than your short term desire to get rich overnight. Trade with no more than 5% of your portfolio and invest the rest in low cost index funds.

6. The power of compounded returns

Compounded returns really make a difference. You may think that 5% – 10% returns are boring, but over the course of decades it stacks up.To understand this concept, Investopedia explains it best in this video:

Let’s run some hypothetical examples.

Example A: $10,000 starting portfolio, $2,000 added per year with a 5% return per year.

After 35 years, total contributions equal $80,000. End portfolio value, $235,800.77. Gross return, +$155,000 (+195%).

Example B: $10,000 starting portfolio, $2,000 added per year with a 9.6% return per year (S&P 500 historical return).

After 35 years, total contributions equal $80,000. End portfolio value, $741,930.11. Gross return, +$661,930.11 (+827%).

Looking at scenario B with a 4.6% higher annual return, the difference is a staggering $506,129.34.

Fun fact: over any 20 year period since 1926, the S&P 500 has never returned a loss.

Lesson: The earlier you can start investing (ideally in low cost index funds), the better. The power of compounded returns over the course of several decades cannot be underestimated.

5. Taking tips from people “smarter” than you is a terrible idea

Hot stock tips are everywhere, and unfortunately no matter how experienced you are, it can be really hard to pass up a great buy tip, especially if the person has apparent access to some “behind the scenes” information no one else knows about.

Unfortunately, ads like the one above for penny stocks are designed to sucker you in to buy a product or service. These tips are utter junk and will leave your wallet and portfolio bleeding red in the end.

Reality: If someone even had a strategy that could consistently return even 11% per year, they’d be rich beyond their wildest dreams and would not need to sell picks.

The S&P 500 historical return is 9.6%. Endowments, pension funds, and the like would poor money hand over fist into any fund manager that could consistently generate 1.4% of alpha decade after decade.

Lastly, this rule includes Wall Street analysts. Ignore analyst buy/sell recommendations.

No one knows what the market is going to do tomorrow, next week, or next year. At best, it’s just an “educated guess” from someone really “smart”.

Warren Buffett sums it up best,

With enough insider information and a million dollars, you can go broke in a year.

Lesson: No matter how smart they are, the odds are always stacked against you. Pursue stock tips with extreme skepticism.

4. One trade can easily make or break your year (or career)

Until you live this first hand, unfortunately it won’t fully hit home. You can spend your whole year seeing small wins and losses. Have an off day, break your rules, and hold a large position into earnings and “wham!”, you might wake up poor the next morning.The opposite is also true. Make a great call, follow your rules, and sell a monster winner that represents over 90% of your gains for the year. Despite dozens or hundreds of uneventful trades over months prior, you’ll be very happy you showed up ready to trade that day.

Lesson: Never underestimate the impact a single trade decision can have on your portfolio.

3. Taxes and the costs of trading are a serious hurdle

This comes back to #9, but it’s worth breaking down the basics. Here are the key terms to understand:- Short term capital gains tax – “Short term capital gains do not benefit from any special tax rate – they are taxed at the same rate as your ordinary income. For 2015, ordinary tax rates range from 10 percent to 39.6 percent, depending on your total taxable income.” – TurboTax

- Long term capital gains tax – “If you can manage to hold your assets for longer than a year, you can benefit from a reduced tax rate on your profits. For 2014, the long-term capital gains tax rates are 0, 15, and 20 percent for most taxpayers. If your ordinary tax rate is already less than 15 percent, you could qualify for the zero percent long-term capital gains rate. For high-income taxpayers, the capital gains rate could save as much as 19.6 percent off the ordinary income rate.” – TurboTax

- Trade Commission – Charge to buy or sell stock.

- Order Execution Quality – Many brokers sell high frequency trading firms the right to “peek” at your order and more or less screw you on your fill. This is called payment for order flow. Despite being $.01 or $.02 per share, poor fill costs can add up real quick when you trade frequently.

Out performing the S&P 500 in any given year is a feat in itself, but when you then take into consideration taxes, commission costs, and research (those hot stock pick services, chat rooms, and market newsletters don’t come for free), the game becomes that much more difficult.

Lesson: When taxes, commissions, and other costs of trading such as research are taking into consideration, the challenge of outperforming the market year after year as a career are compounded.

2. Confirmation bias and your emotions are your worst enemy

Trading is a mental game. The mind is a beautiful thing, and given a runway of endless inspiration data, it can wreak some serious havoc.

Confirmation bias definition via Wikipedia,

Confirmation bias is the tendency to search for, interpret, prefer, and recall information in a way that confirms one’s beliefs or hypotheses while giving disproportionately less attention to information that contradicts it.

In the trading world, this means you see a setup or price action and quickly convince yourself to buy or sell. Unfortunately, 99% of the time you should be doing the direct opposite.

Technical analysis is one of the worst in provoking this natural human behavior. “Oh, I’ve seen this pattern before, it’s a buy”. There is a reason why online brokers offer dozens and in some cases hundreds of technical indicators. Indicators encourage you to see more “patterns” and trade more frequently.

In poker, a player can go on “tilt” and make poor decisions, ultimately losing their stack in a hurry. The same mental dilemma applies to trading.

Several quotes from market masters on trading psychology,

- The truth is that trading, both successful and unsuccessful, is more about psychology than tactics. – Jack Schwager

- I’m always thinking about losing money as opposed to making money. Don’t focus on making money, focus on protecting what you have. – Paul Tudor Jones

- Everyone has the brainpower to make money in stocks. Not everyone has the stomach. – Peter Lynch

Lesson: Trading is 90% mental and 10% skill. Those who succeed learn to manage risk and trade unemotionally.

1. Passive indexing is the best path forward for 99.9% of Americans

Widely regarded as the greatest investor of all time, Warren Buffet understands the market and his advice for the average American is priceless:

It is not necessary to do extraordinary things to get extraordinary results. … By periodically investing in an index fund, the know-nothing investor can actually outperform most investment professionals.

Historically speaking, since 1928 the S&P 500 has returned 9.6% per year. By simply buying an ETF like SPY or VOO, you can replicate the performance of the S&P 500 for .09% or .05%, respectively, in expense ratios per year. The same applies for mutual funds like Vanguard’s VFIAX.

As far as allocation goes, Warren also keeps it simple,

My advice to the trustee could not be more simple: Put 10% of the cash in short-term government bonds and 90% in a very low-cost S&P 500 index fund. I suggest Vanguard’s. (VFINX)

The numbers don’t lie. Despite staffs of analysts, access to CEOs, CFOs, unlimited capital for research, etc. on average, the majority of hedge funds underperform the market each year.

For a detailed guide on passive indexing like Warren Buffett, see How to Build a Warren Buffett Portfolio.

Lesson: Warren Buffett is the greatest investor of all-time. He recommends low cost indexing, instead of market timing, as the best path to long term success.

Closing Thoughts

For new investors getting started, trading should be a quest for knowledge, not about getting rich.While I have no regrets of investing thousands of hours into the markets over the past 14 years, I’ve had to accept the reality that my retirement portfolio would be further ahead had I understood these truths from the beginning:

- The “lifestyle” of a pro trader is a big fat lie

- You really need at least a $1,000,000 portfolio to trade full-time

- The odds are stacked against you

- Allocate 5% or less of your portfolio to trading and invest the rest in low cost index funds

- The effect of compounded returns over the course of several decades is amazing

- Taking tips from people “smarter” than you is a terrible idea

- One trade can easily make or break your year (or career)

- Taxes and the costs of trading are a serious hurdle

- Confirmation bias and your emotions are your worst enemy

- Passive indexing is the best path forward for 99.9% of Americans

If your mentality is to use the market as a vehicle to supplement income or get rich because you don’t see your personal career getting you where you want to be, stop yourself, you’re already primed for failure.

SOURCE: stocktrader.com/